Romania's Retail Sector: Trends and Outlook for Q2 2026 May 2026

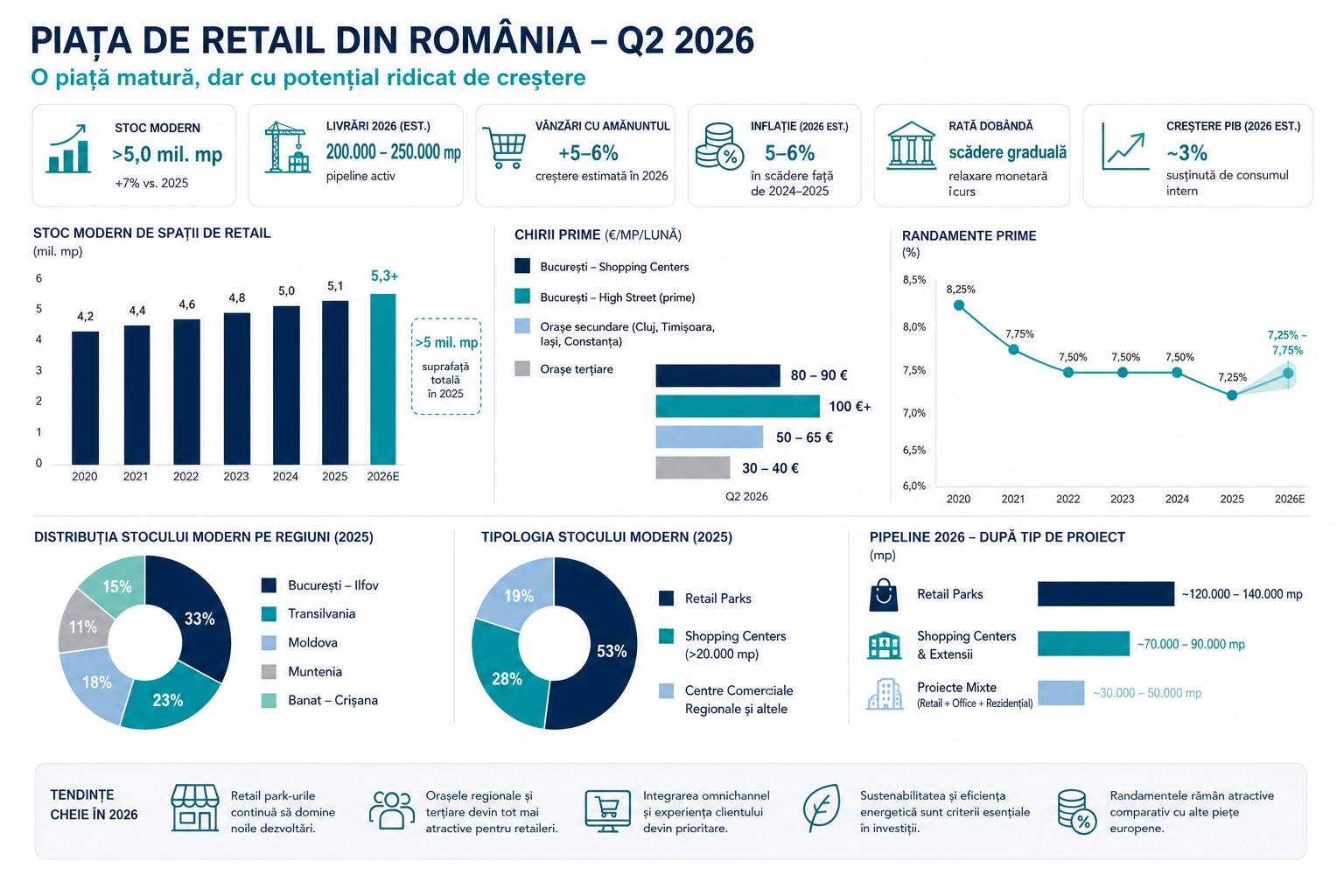

Romania’s retail sector enters Q2 2026 in a clear phase of maturation, characterized less by rapid expansion and more by optimization, strategic selection, and consolidation. After an intense development cycle between 2017–2023, the market has surpassed the threshold of 5 million square meters of modern retail space, while the pace of deliveries remains solid, with approximately 200,000–250,000 sqm scheduled for 2026.

In this context, Romania continues to be one of the most dynamic retail markets in Central and Eastern Europe, but also one of the least saturated, which sustains the interest of international investors.

From a macroeconomic perspective, fundamentals remain relatively solid. Inflation has moderated compared to previous peaks, stabilizing in the 5–6% range, while monetary policy is beginning to enter a phase of gradual easing. Economic growth is estimated at around 3% for 2026, primarily supported by domestic consumption. However, this growth is more moderate, and consumers are becoming more price-sensitive, which explains the strong performance of value and discount retailers. This type of behavior directly influences tenant expansion strategies and the typology of developments.

One of the most evident trends in 2026 is the strengthening role of regional cities. Urban centers such as Cluj-Napoca, Timișoara, Iași, and Brașov continue to attract major investments, but the gap compared to tertiary cities has narrowed significantly. Locations such as Sibiu, Oradea, and Alba Iulia are becoming increasingly relevant on developers’ maps, particularly for retail park formats. This more balanced distribution reflects both the growing purchasing power outside the capital and a more cautious investor strategy focused on stable yields and lower development costs.

On the demand and supply side, the market is shaped by a clear structural shift: retail parks have become the preferred product. They offer flexibility, lower operational costs, and better alignment with current consumer behavior. At the same time, large shopping centers remain relevant, but their development is far more selective and concentrated in dominant, super-regional schemes. Large-scale projects such as those in Iași or Cluj-Napoca reflect this direction, where retail is increasingly integrated into mixed-use developments alongside office and residential components.

Rental levels in 2026 confirm the market’s maturation. In Bucharest, prime rents in dominant shopping centers range between €80–90/sqm/month, while the premium high street segment exceeds €100/sqm/month in top locations. In secondary cities such as Cluj-Napoca, Timișoara, or Iași, levels remain relatively stable between €50 and €65/sqm/month, reflecting a healthy balance between supply and demand. In tertiary cities, rents generally range between €30 and €40/sqm/month, with a slight upward trend driven by increasing retailer interest in these markets. Prime yields remain competitive at a regional level, within the 7.25% – 7.75% range, continuing to position Romania favorably compared to other European markets.

At the same time, retailer behavior is visibly evolving. Expansion continues but is more carefully calibrated, with a stronger focus on operational efficiency and the performance of each location. The food & beverage, entertainment, and services segments are gaining increasing importance, transforming shopping centers into leisure destinations, not just shopping spaces. The integration of online and offline channels is becoming standard, while investments in technology and customer experience are essential for competitiveness.

Looking ahead, the outlook for the next 12–24 months points to moderate but healthy growth. Continued expansion in secondary and tertiary cities is expected, along with limited upward pressure on rents in dominant locations and sustained interest from international investors attracted by yields that remain above the European average and by the market’s growth potential. At the same time, project selection will become more rigorous, and the gap between high-performing and secondary assets will widen.

In conclusion, Romania’s retail sector in Q2 2026 is no longer defined by rapid expansion, but by maturity and investment discipline. For investors, the opportunity no longer lies simply in entering the market, but in choosing the right product and location. Romania remains a market with attractive yields and growth potential, but success increasingly depends on strategy, not just timing.